Economic Outlook and Portfolio Review2023 Year-end Review

- johnfmarkham

- Jan 11, 2024

- 15 min read

2023: A Year to Remember

Well, what can we say about 2023? It’s been a bit like one of those mystery novels you can’t put down. Just when you thought you had it all figured out, the plot took another twist.

2023 certainly threw us a curveball in the world of finance, demonstrating that the only sure thing about the economy and markets is their unpredictability. Back in December 2022, Bloomberg called upon the elite of Wall Street, including powerhouses like J.P. Morgan and Goldman Sachs, to cast their forecasts for the upcoming year. The consensus among these seasoned analysts was a rather conservative 7% return for the S&P 500 for the year ahead. Yet, as the year unfolded, it was clear that 2023 had its own script, decidedly more optimistic than the experts' forecasts. The U.S. market didn't just progress; it surged, notching a remarkable 22.1% gain.

Then there’s the bond market, which had an interesting year in 2023. It started off sluggish, almost like a bear waking up from a winter nap. But as the year progressed, it picked up steam, ending on a high note that surprised many of us. A significant factor behind this change was the global central banks getting a better handle on inflation. Their efforts to tame inflation seemed to pay off, bringing a sense of relief and stability, which in turn provided a nice boost to the bond market.

Now, no year is complete without its share of drama. The first quarter had us all on the edge of our seats with a global financial scare. The fall of Silicon Valley Bank set off a domino effect, but thankfully, governments stepped in just in time to steady the ship. However, we did wave goodbye to the independence of Credit Suisse, which found a new home with UBS.

On a different note, 2023 also saw a few breakthrough events, starting with a leap in space exploration as India achieved a historic moon landing, marking a significant milestone in its space program. This celestial success was mirrored on Earth by healthcare breakthroughs, notably in weight loss drugs like Ozempic, which gained celebrity endorsement and, surprisingly, showed potential in Alzheimer's research. Who knew a financial report would touch on weight loss trends?!

But 2023 has also been a year where we had to celebrate the life of an investment legend in his 100th year. Charlie Munger, known for his wit and wisdom, left us with invaluable insights, one of which perfectly encapsulates our approach: 'The big money is not in the buying and the selling, but in the waiting.' His legacy inspires us, reminding us that patience and a long-term perspective are vital to achieving your financial goals.

So, please grab a cup of your favourite drink, and let’s dive into the details of this incredible year.

Economic Outlook and Market Commentary

The Battle Against Inflation Has Made Significant Progress

As we moved through 2023, the relentless battle against rampant inflation continued across various economies. Despite widespread fears of a looming global recession at the year's start, central banks stood firm, implementing and upholding elevated interest rates. To the surprise of many, several economies have shown resilience, with inflation becoming less ingrained than feared.

In the US, the economy showcased its fortitude, sidestepping the dire predictions of collapse. The annual inflation rate eased to 3.1% in November, a notable decline from 7.1% recorded in the same month last year. A significant contributor to this downtrend was the 5.4% fall in energy costs during November, playing a substantial role in curbing overall inflation. Additionally, core inflation, which strips out volatile food and energy prices, aligned with expectations at 4%. The ebbing inflation in the US, and projections of this trend's persistence into 2024, have invigorated the stock market and bolstered hopes for a gentle economic descent.

Meanwhile, the UK witnessed its inflation rate dip from 4.6% to 3.9% in November, hitting a two-year low. The Office for National Statistics attributed this sharper-than-anticipated fall primarily to decreasing petrol prices and moderating food and household goods prices. Yet, this rate still hovers nearly double the Bank of England's 2% target, maintaining elevated pressure on household budgets and business finances.

Compared to the broader European landscape, the UK's inflation rate stands on par with France's but still exceeds the eurozone's average of 2.4% . The panorama in Europe may look promising, yet the prospect of interest rate reductions is not imminent, as lingering concerns persist - concerns that also shadow other developed markets. Wage inflation, typically slower to react to shifts in inflation, could dilute the impact of high interest rates. When examining the third quarter of 2023 against the previous year, wage increases in the eurozone are approximately 5%. The UK's annual regular pay growth hit 7.3% in October, while the US saw a 5.2% rise.

With Recession Risks Still Looming, Markets Are Anxious For Rate Cuts

With inflation heading in the right direction, central banks on both sides of the Atlantic have come under renewed pressure to cut interest rates in the new year. For investors and market analysts, the pulse of the broader economy, measured by an array of indicators, is of even greater consequence than any single inflation statistic.

Globally, we're seeing a sluggish pace in productivity growth, which naturally caps the potential for GDP expansion. Labour markets remained strained throughout 2023, suggesting minimal scope for further employment gains. In the UK, third-quarter GDP unexpectedly contracted by 0.1%, veering away from initial forecasts of stagnation4F . With a consecutive contraction in the fourth quarter looking increasingly likely, the spectre of a technical recession looms.

The eurozone, too, witnessed a slight dip, with seasonally adjusted GDP down by 0.1% in the third quarter5F . Germany, the bloc's economic powerhouse, has been particularly hard hit by surging energy costs and heightened competition from imported Chinese vehicles. The European Central Bank’s (ECB) ongoing monetary tightening is also exerting pressure, with anticipated annual real GDP growth decelerating from 3.4% in 2022 to a modest 0.6% in 2023 and only a slight uptick to 0.8% forecast for 2024. This starkly contrasts the approximately 2% growth rates seen in the pre-pandemic era .

A critical debate now centres on the timing of interest rate reductions. The Bank of England has raised rates 14 times since December 2021, peaking at a 15-year high of 5.25% by the end of 2023. Governor Andrew Bailey has cautioned that more needs to be done to meet the inflation target before rates can fall. Despite this, many economists are now predicting rate cuts in the UK as early as the first half of 2024. Similarly, on December 14th, the ECB quashed any speculation of immediate rate reductions by committing to maintain elevated borrowing costs despite the softening of inflation forecasts. This stance has heightened market apprehension, with several economists and leading figures arguing for prompt rate cuts to preclude the necessity of more drastic measures later in 2024.

In stark contrast, the Federal Reserve in the US is signalling a more optimistic outlook, as reflected in the stock market's robust performance. The US economy has exceeded expectations in terms of GDP and employment, with an anticipated growth of 2.4% this year - 2 percentage points above what was forecast a year ago. The unemployment rate edged down to 3.7% in November. Consequently, analysts are revising their projections for the US economy's future upward, with Goldman Sachs estimating just a 15% chance of a recession in 2024 .

The question then arises: Why the rush for rate cuts in a seemingly flourishing American economy? One reason is that the full effects of high interest rates often take time to permeate the market. To sustain economic health into late 2024 and beyond, timely adjustments to interest rates are essential. Additionally, the US budget deficit has ballooned in 2023, and the persistently high interest rate environment amplifies concerns over debt sustainability under any given tax or spending framework. Corrective actions are necessary to avert a prolonged escalation in the cost of servicing US government debt.

Most analysts are now predicting a series of rate cuts for the US federal funds rate in 2024, ranging from six to eight quarter-point reductions, totalling a decrease of 150 to 200 basis points. Should this transpire, the current peak rate of 5.5% in the US could settle to approximately 4% by year's end.

Looking Ahead: Interest Rates in the New Economic Landscape

In essence, as central banks become more confident that inflation is inching towards their desired levels, most financial experts foresee a scaling back of policy interest rates beginning in 2024. Yet, there's a variety of opinions on when we'll witness the first decrease.

What's broadly agreed upon is that interest rates are expected to find a new normal at heights we haven't seen since before the Global Financial Crisis and the COVID-19 pandemic, periods when they were exceptionally low. We're observing a climb in what's known as the natural rate of interest or r-star. Picture this rate as the economy’s “just-right” temperature - it's the sweet spot where the economy hums along steadily without the engine of inflation overheating.

This gradual uptick is driven by major forces such as shifting demographics, ongoing improvements in how effectively we work, and more substantial government budget deficits. The critical point to grasp is that we appear to be on the verge of a period characterised by generally higher interest rates. This substantial and lasting transformation is likely to be a defining force in shaping the economic and financial narratives in the foreseeable future.

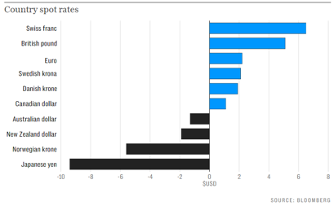

Sterling Emerges Victorious: Dominating the 2023 Currency Landscape

In 2023, the British Pound stood out in the currency markets, proving to be one of the strongest performers among the major global currencies. For those exchanging Pounds, the value against the Dollar improved from $1.21 to $1.27 for every £1. The story was similar with the Euro, where £1 increased in value from €1.13 to €1.16, making trips to the continent slightly more budget-friendly.

But it wasn't just holidaymakers who benefited from the Sterling's strength. A stronger Pound contributed to easing inflation by reducing the cost of imported goods. The bolstered Pound also supported domestic investments and assets hedged to the Pound, supporting their return.

The Pound’s rise can largely be traced back to a stronger-than-anticipated economy and the Bank of England's proactive interest rate hikes, which drew in international investors enticed by the promise of higher returns. The chart below showcases the 2023 currency performance of the G10 countries relative to the Dollar. As illustrated below, the British Pound was only outperformed by the Swiss Franc, highlighting its prominent position in last year’s currency landscape.

Asset Class Returns

A Year-end Review with a Ho-Ho-Whole Lot of Growth

As we say goodbye to 2023, it's been like ending on a high note with an unexpected bonus track. What played out towards the end of 2023 is known as a Santa Claus rally. Just when we thought the year was done, the markets gave us a parting gift. There are a bunch of theories about why it happens; some say it's the seasonal joy, others think it's those year-end bonuses burning a hole in investors' pockets, and a few just chalk it up to the bigwigs being away, letting the market play. Whatever the reason, it's a nice way to round off the year.

As we turn the last page of 2023, the financial narrative has been one of a remarkable rebound across the board for asset classes, painting a stark contrast to the preceding year. Equities have been the stars of the show, with developed markets leading a charge that has seen the sector's valuations soar, particularly in the U.S., where investors have witnessed returns that far outstrip those seen in the last five years. Bonds, often seen as the steadier hand, shook off the extreme volatility of 2022 and advanced towards stability and growth as the year came to a close, buoyed by a collective sigh of relief as central banks signalled a more accommodative stance.

The narrative for real estate, while varied throughout most of the year, ended on a positive note, as the sector clawed back into favour towards the year's end, suggesting potential for continued growth into the next. In contrast, the journey for emerging markets remained complex, with these equities delivering a mixed performance, reflecting these economies' nuanced and often unpredictable nature.

Equities

The Magnificent 7

Reflecting on the equity landscape of 2023, we saw an extraordinary tale of dominance and performance. This story stars a group of companies so influential they've been dubbed the 'Magnificent Seven.' Evolving from the legacy of the FAANGs, this group, which includes tech giants like Meta, Amazon, Apple, and Alphabet, alongside Microsoft, Tesla, and Nvidia, has left an indelible mark on the year's stock market narrative.

The illustration below showcases the performance of the 'Magnificent Seven,' with Nvidia, Meta and Tesla leading a meteoric rise.

The influence of these behemoths extends beyond mere percentage points. Collectively, they command a market presence with their combined economic weight challenging the combined weight of countries like Canada, France, China, the UK and Japan.

The market clout of these seven titans is evident as they've steered the U.S. market's performance. The chart below shows the stark contrast between the 'Super Seven' - soaring with a 74% rise - and the rest of the U.S. market, which saw a more modest 12% growth. Their significant impact on market trends is unmistakable.

For many investors, the concentration of wealth in these 'Magnificent Seven', or in U.S. equities as a whole, may raise concerns about concentration risk. Indeed, putting too many eggs in one basket, even if it's a basket holding some of the most successful companies, can be a precarious strategy. On the flip side, one can also argue that there is a risk in not holding these stocks, given their substantial contributions to market performance.

We consistently advocate for a diversified investment approach. While valuations in the U.S. are notably high, we've observed that such valuations can persist for longer than anticipated, and missing out on potential gains is a risk in itself. Therefore, we see global market capitalisation diversification as a point of great diversification - where the markets have balanced risk and reward and where supply meets demand harmoniously.

That said, for investors who are inclined to spread their wings beyond the substantial influence of the 'Magnificent Seven,' we recommend a reshaped index that leans into known risk factors such as value and small-cap stocks. This underpins our investment philosophy, providing a structured approach to diversification that acknowledges market realities while striving for robust performance.

Risk Factors Showing Promising Returns

Many investors have felt the strain when it comes to value stocks in recent years, often pointing to them as the culprits in a factor-based portfolio's lagging performance. They've been somewhat the scapegoat, the black sheep, if you will. Yet, a closer look reveals that value stocks have demonstrated remarkable resilience over the last three years.

In the past three years alone, Global Value stocks boasted a 38.35% return, outdoing the 26.41% of global equities. This rebound underscores the cyclical nature of the markets, affirming that patience can indeed lead to prosperity and that what goes down may well come up.

Small-cap stocks have similarly been recalibrating in the background, and as 2023 came to a close, they surged with an 8.67% return in the fourth quarter, eclipsing both global equities and value stocks. Though not topping the charts, their one-year and three-year performances suggest a resurgence in form. The recent uptick may well herald a broader revival for small-caps, underscoring their potential for long-term growth in a diverse portfolio.

The forthcoming charts illustrate the returns of Value and Small-cap stocks in relation to global equities over three years, one year and specifically for Q4 2023, illustrating their encouraging recovery.

Ⓒ Timeline Holdings Ltd 2024: All data is up to latest available price. Past performance is no guarantee of future return. The data is sourced from Morningstar API, for which we are not responsible. Where Morningstar may have missing data or inaccurate data, we are not responsible. Careful consideration has been taken to ensure that the information is correct but it neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, Inaccuracies, omissions or any inconsistencies herein. Percentages may not total 100 due to rounding. Performance figures are net of fund manager charges. This tracking error is calculated by Morningstar over a 10-year period and then annualised. Where tracking error is not displayed, the comparable index was not available in Morningstar Direct in order to calculate.

The data for the indices and the underlying funds of the portfolios is sourced from Morningstar API. We are not responsible for their presence or accuracy.

This chart shows the cumulative performance % of the selected financial assets from the starting point. You have to hover over a specific month to see the cumulative performance that the asset had from the starting point up to that month.

Emerging Markets Still Struggling On

The past year has painted a complex picture for emerging markets, which have experienced modest growth relative to the more pronounced advances in developed markets. The chart illustrates a clear contrast, with developed markets soaring by 20% in cumulative performance while emerging markets have seen a relatively subdued rise of 3.69%. This performance gap reflects the challenges emerging markets often face, from political instability to less mature financial systems, which can deter the kind of robust investment inflows that developed markets typically enjoy during periods of economic stress.

Despite this overall lag, emerging markets have shown signs of positive momentum. The latter part of 2023 marked a turning point as the dovish tilt of the Federal Reserve provided a much-needed boost. This change in stance by one of the world's major central banks has given investors renewed confidence, spurring a rally that suggests emerging markets are far from stagnant.

Fixed Income

2023 was a year of grit and endurance for fixed income investors, marked by a challenging start but ending with a historic rally that reinvigorated the fixed income landscape with fresh optimism.

Initially, bond prices waned under the heavy cloud of ongoing rate hikes by central banks aimed at curbing inflation. This sentiment hit a low in October when U.S. Treasury yields breached the 5% mark, a level not seen in over 15 years9F , echoing a similar slump for UK government bonds to a nadir last observed in 2008. These trends signalled a potential third year of losses for bond funds, a streak unseen in almost forty years.

But the narrative shifted dramatically in November. As inflationary fears began to ease and whispers of impending rate cuts grew louder, investors quickly pivoted back to treasury bonds. This shift sparked a significant rally, culminating in a solid year-end performance. The Bloomberg Global Aggregate Total Return Index surged, notching up its best two-month streak since 1990 with nearly a 10% gain.

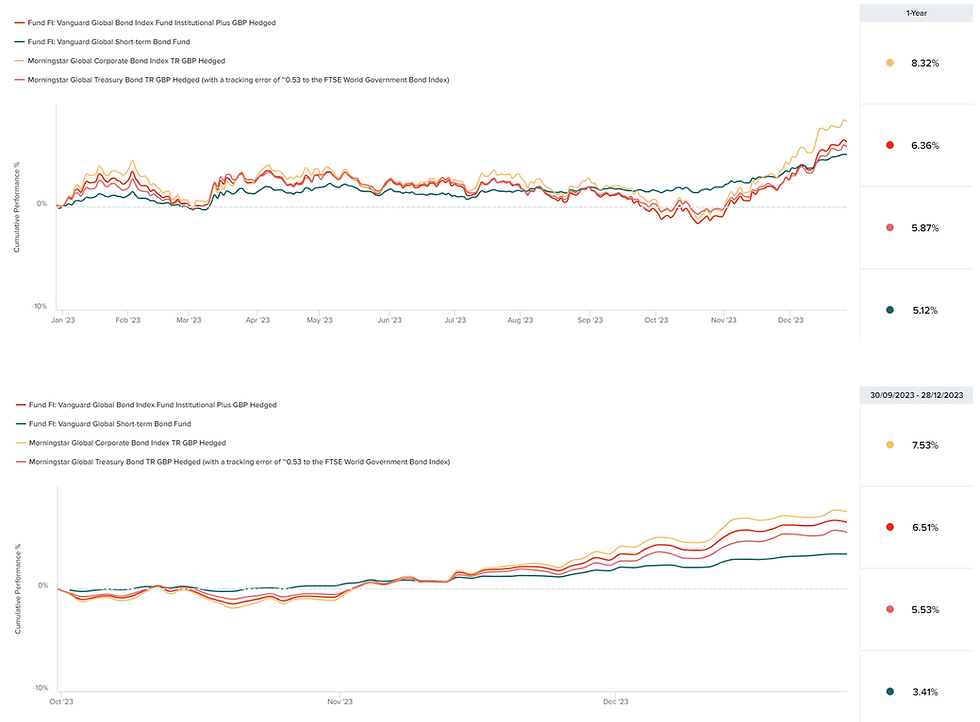

The following charts reflect this tumultuous journey for various segments of the bond market over three years, one year, and specifically, the fourth quarter of 2023.

• Global bonds, as represented by the Vanguard Global Bond index fund, receded by 10.29% over three years, yet rallied to regain 6.36% in 2023, with an impressive 6.51% recovery in the last quarter alone.

• Short-dated bonds, less sensitive to interest rate changes and represented by the Vanguard Short-dated bond fund, showed resilience, down only 1.73% over three years. They bounced back with a 5.12% increase in 2023 and a 3.41% uplift in the final quarter.

• Global Government Bonds, after a three-year dip of 9.65%, recovered with a 5.87% rise in 2023, partly thanks to a 5.53% increase in Q4.

• Corporate bonds, while down 9.60% over three years, enjoyed a resurgence of 8.32% in 2023, with a significant 7.53% of that growth coming in Q4.

As expectations mount for a downtrend in interest rates, fixed income assets are well-positioned to recoup losses. Moreover, with yields currently above average, these assets offer attractive coupons, making fixed income a compelling diversifier against equity risk.

Real Estate

REITs, or real estate investment trusts, have had their share of ups and downs over the last three years, facing unique challenges that have left them trailing behind the broader global equity market. When we look at the numbers, global equities have been on a tear, with a three-year gain of over 26%, while REITs have posted a more modest increase of nearly 8%. Just in the past year, while global stocks have jumped by more than 16%, REITs have seen a rise of only 5%.

So why have REITs been lagging? Well, rising interest rates have made it more costly for them to operate since they often rely on debt to grow. The pandemic's after-effects have also hit them hard, especially with many of us shopping online more and going into the office less, reducing the demand for both retail and office spaces. Plus, the hospitality sector within REITs has been slow to bounce back, with travel taking a hit.

But it's not all gloomy. The last quarter of 2023 brought some hope, with REITs increasing by about 6.5%. It seems like there might be a light at the end of the tunnel as the market starts to adapt to the new normal and REITs begin to adjust to the shifts in how we use spaces. It's been a bumpy ride, but these signs of recovery could spell better days ahead for real estate investments.

Final Thoughts

Reflecting on the past twelve months, it’s clear that 2023 was a year for the books - a year when markets soared beyond the most optimistic of Wall Street forecasts. This unexpected leap serves as a powerful reminder that, despite our best efforts to forecast, the markets will always be defined by their dual nature of unpredictability and potential for long-term growth.

As we peer into the landscape of 2024, it's apparent that it's not just market forces that will command our attention, but the political stages across the world as well. A series of key elections are on the horizon - from the pivotal presidential race in the United States that could shape global economic policies, to the UK's potential parliamentary showdown, Taiwan's critical elections that may influence technological and geopolitical arenas, and South Africa's national elections that could herald a new era of governance. Each of these political milestones is expected to generate its share of headlines and market volatility, contributing to short-term noise that could distract even the steadiest of investors.

However, it's crucial to remember that our focus should not waver from the long-term trajectory of the markets. Historical trends remind us that while elections can stir the waters, the underlying currents of market progress continue to flow unabated. Staying the course, adhering to our well-crafted strategies, and maintaining a clear vision for the future will enable us to navigate through any temporary upheaval with confidence.

Bibliography

Bank of England. (2023, September 21). When will inflation come down in the UK? Retrieved from https://www.bankofengland.co.uk/explainers/will-inflation-in-the-uk-keep-rising#:~:text=We%20expect%20inflation%20to%20fall,the%20first%20half%20of%202025.

Bloomberg. (2023, December 28). global-bonds-eye-biggest-ever-two-month-gain-amid-rate-cut-bets. Retrieved from Bloomberg.com: https://www.bloomberg.com/news/articles/2023-12-28/global-bonds-eye-biggest-ever-two-month-gain-amid-rate-cut-bets

British Broadcasting Corporation (BBC). (n.d.). UK interest rate freeze ends run of 14 straight increases. Retrieved from https://www.bbc.co.uk/news/business-66875739

Bureau of Labor Statistics . (2023, 12). https://www.bls.gov/news.release/laus.nr0.htm. Retrieved from https://www.bls.gov/ : https://www.bls.gov/news.release/laus.nr0.htm

European Central Bank (ECB). (2023, September 14). Monetary Policy Decisions. Retrieved from https://www.ecb.europa.eu/press/pr/date/2023/html/ecb.mp230914~aab39f8c21.en.html

European Central Bank (ECB). (2023a, September 15). Press Conference: Christine Lagarde, President of the ECB, Luis de Guindos, Vice-President of the ECB. Retrieved from https://www.ecb.europa.eu/press/pressconf/2023/html/ecb.is230914~686786984a.en.html

eurostat - European Commission. (2023). Euro area annual inflation down to 2.4%. European Commission.

Eurostat. (2023, September 19). Euro Indicators. Retrieved from https://ec.europa.eu/eurostat/web/products-euro-indicators/w/2-19092023-ap#:~:text=The%20euro%20area%20annual%20inflation,%2C%20the%20rate%20was%2010.1%25.

Federal Reserve (Fed). (2022, August 26). Speech: Monetary Policy and Price Stability (Chair Jerome H. Powell). Retrieved from https://www.federalreserve.gov/newsevents/speech/powell20220826a.htm

Federal Reserve (Fed). (2023, August 25). Speech: Inflation: Progress and the Path Ahead (Chair Jerome H. Powell). Retrieved from https://www.federalreserve.gov/newsevents/speech/powell20230825a.htm

Federal Reserve Bank of Atlanta. (2023, 12). Wage Growth Tracker. Retrieved from www.atlantafed.org: https://www.atlantafed.org/chcs/wage-growth-tracker

Goldman Sachs. (2023). 2024 US Economic Outlook: Final Descent (Mericle) . Goldman Sachs Economics Research.

International Monetary Fund. (2023). One Hundred Inflation Shocks: Seven Stylized Facts. Working Paper. Retrieved from https://www.imf.org/-/media/Files/Publications/WP/2023/English/wpiea2023190-print-pdf.ashx

Office for National Statistics . (2023, 11). Inflation and price indices. Retrieved from https://www.ons.gov.uk/: https://www.ons.gov.uk/economy/inflationandpriceindices

Office for National Statistics. (2023, September 29). GDP quarterly national accounts, UK: April to June 2023. Retrieved from https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/quarterlynationalaccounts/apriltojune2023

Comments